Accenture is the world’s largest IT services company with $69.7 bn in FY’25 revenues and 779,000 employees. They serve 9000+ clients with a presence across 52 countries. It is one of the most admired companies in the world with the strongest brand value amongst all IT services companies. Local currency growth in Q1 FY’26 was 5%. Accenture is betting big on Data and AI as referenced by setting up of an Anthropic Business Group with 30k people, a strategic partnership with Palantir and majority stakes in companies building AI datacenters.

Accenture has a very strong local presence in BeLux with a long history, top notch client portfolio and more than 1300 local employees. With the acquisition of Arηs (pronounced Aris) in July 2024, Accenture added another 2100 people to its BeLux workforce. With 2500 people (the other 400 being in Greece) Arηs is a significant and well respected player within the European Institutions. With this acquisition, Accenture is now part of a large number of the European Framework Agreements. While most of Arηs activity is application development (Java, .Net), they also have capabilities around datacenter/cloud and end user services.

Accenture is praised by clients for its business understanding, transformation capabilities, and ability to bring and apply global knowledge for its clients. Despite its extensive size and global presence, it works as one integrated organization with a uniform way of working.

Accenture is present in three out of our four squares. They area leader on two squares: Applications & Digital and Security services.

Applications & Digital

Accenture continues to be a Leader within our Applications & Digital square with the highest Market Impact score and a strong CSAT of 3.75 (consistent with last year). They have very strong capabilities across Systems Integration, Applications Management and Digital Transformation and had the maximum number of data points of any service provider with 24 clients. The Arηs acquisition makes them the largest player in this space locally.

Cloud & Datacenter

Accenture’s cloud and datacenter capability comprises of Sentia, Avanade (Azure) and its homegrown cloud and datacenter capability. They are positioned as a Strong Contender with a CSAT of 3.45 (up from 3.29 last year). Sentia brought a strong hybrid cloud capability in the BeNeLux with 400+ people. They have a best-in-class capabilities for cloud control and optimisation, backed up by a strong service catalogue. They specialize on Azure and AWS with 5 availability zones in BeNeLux. They also have a strong Digital Experience Monitoring capability. Accenture-Sentia will be a very strong fit for mid-tier clients who want local expertise. The challenge for Accenture is the extension of this niche local capability across their offshore delivery centers and into their larger clients.

Cybersecurity

Accenture is one of the leading cybersecurity providers in the world with more than 27,000 professionals and $10bn in global revenue. They come out as a Leader on our security square due to the size of their local security business and mature capabilities. They are very strong on security advisory and implementation (roughly half of the business). They have an extensive network of security operations and delivery centres and Cyber Fusion centres focused on offensive security. Accenture are particularly strong in their identity and access management practice and have invested significantly on the application of AI in cyber security. They had a CSAT of 3.87 (up from 3.66 last year).

Main Sectors

-

Large & Medium enterprises across all verticals

# Contracts

45

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

Cybersecurity

✓

POSITIVES

-

Deep business understanding

-

Consulting / transformation orientation

-

Strong local capability and workforce

NEGATIVES

-

Contracting and negotiation is more difficult

-

Strong culture is sometimes conflicting with clients

-

Premium pricing

Atos has 67,000 people across 61 countries, supporting 2700 clients. In FY 2025, Atos group expects to generate €8.5 bn in revenues. By the end of January 2026, Philippe Salle would have achieved what his 3 predecessors could not – stay on as CEO for a full year! Under his leadership, Atos initiated the 4-year Genesys transformation plan aimed at delivering revenues of €9-10 bn and operating margin of 10% by 2028. The recent divestments – Ideal GRP in the Nordics and the sale of the entire south America business and ongoing workforce reduction are part of this program. An overall book to bill ratio of 66% (even if aligned with the Genesys strategy) remains worrying.

While calm seems to be returning to at the corporate headquarters, Atos BeLux continues to perform well in a difficult market. Atos BeLux is part of the wider Atos Noridcs, and under the leadership of Punit Sehgal has been the best performing BU for the last two years. In 2025 they had some particularly large wins at the European Commission (300mn+) and Digipolis (100mn+) demonstrating renewed confidence in the company.

Atos is one of five companies in our survey who are present in all four squares. They are a world leader in the areas of supercomputers, cybersecurity and managing global sports events. Atos is particularly strong within the European Institutions and public sector.

Applications & Digital

Atos develops and operates modernized business application platforms. They offer for systems integration and applications management capabilities across custom platforms and packaged applications. They have a strong capability on Analytics through their BDS division.

Cloud and Datacenter

Atos operates critical business workloads from the edge to the public cloud. They have their own private cloud solution, operate datacenters, manage networks and supercomputers. They are one of the leading mainframe operators in the world. They sit within the Strong Contenders category.

End User Services

Atos has a strong end user services capability that offers multilingual support from Tenerife and central eastern Europe. They operate what is probably the largest end user services contract in BeLux at the European Commission. They sit high within the Strong Contenders category.

Cybersecurity

Atos is a leader in cyber security services globally. With 6000+ security consultants it offers end to end security services for digital identity, cloud security, IoT security, ADR and data privacy. Their acquisition of digital.security in 2020 cemented their status as a leading security supplier in BeLux. They operate state of the art SOCs and have their own patented platform AIsaac which is widely deployed. Atos drops from the Leaders category this year due to reduced CSAT.

Main Sectors

-

Large & Medium enterprises

-

Government / EU

# Contracts

46

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

✓

POSITIVES

-

Strong track record and capabilities in Cloud / DC and Security

-

Deep understanding of EU / public domains

NEGATIVES

-

Returning to growth and profitability is a challenge

-

Perception amongst non-Atos clients

Capgemini is a global applications & technology and engineering services firm with €22.1 bn in 2024 revenues (down 2%), and expects to grow between 2-2.5% in 2025. The growth comes from outside of France and Rest of Europe, as these two regions are contracting this year. Capgemini has 354,000 people across 50 countries. They have a strong focus on Europe (62% of revenues) and Belux (local workforce of ~2500). They are also well represented in all the industry sectors and government organizations.

They are one of five firms in our survey who are represented on all four squares. Their 3 main service lines are: Strategy & Transformation (9%), Applications and Technology (62%) and Operations & Engineering (29%). They are able to seamlessly blend their offshore capability for support and operations, with its local workforce for consulting, transformation and local client interfacing. Capgemini Engineering is one of the leaders in product engineering.

In 2025, Capgemini acquired WNS, a leader in the BPO space paying €4 bn and betting big on the potential of AI powered business process services. WNS had revenues of $1.27 bn and 9% growth in the last three years.

Applications & Digital

Capgemini continues to remain a Leader for Application & Digital Services with a CSAT score of 3.77 (consistently high since the last 3 years) measured across 17 clients. This assessment comes on back of the strength of their local business, maturity and completeness of service offering and high customer satisfaction scores. They have strong capabilities in SAP and are a leader in S/4 HANA transformations across Europe. They are one of the few companies to have a strong focus on testing services and low-code no-code applications.

Cloud and Datacenter

Capgemini appears as a Challenger on our Cloud & Datacenter square. This year they have made a strong improvement on the CSAT score with a score of 3.58. While they have strong capabilities in this area globally, they are underrepresented on the BeLux market.

End User Services

Capgemini has a strong end user services capability leveraging their nearshore and offshore capabilities. Their vision for workplace of the future and capability in Poland comes in for praise from their clients. CSAT on this square has also improved significantly with a score of 3.37 (versus 3.07 last year)..

Cybersecurity

With 6,000+ experts and network of 13 cyber defence centers and SOCs, Capgemini is a global leader for the provision of security services. Their security offerings include advisory, implementation, MDR and pen testing. They are a leader in IoT and industrial security skills and cloud security. In BeLux they provide MDR and pen testing services for a large number of customers. They had an even better CSAT of 4.05 (compared to 3.80 last year) and sit within the Strong Contenders category for this square.

Main Sectors

-

Large & Medium enterprises

-

All sectors

# Contracts

35

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

✓

POSITIVES

-

Very good mix of global and local capability

-

Capabilities across the entire IT stack

-

Flexibility and cultural alignment

NEGATIVES

-

Under-represented on Cloud-DC and End User Services

Cegeka is a Belgium based international IT services company with revenues of €1.3 bn and 9000 employees. What started as a small Belgian company 30 years ago, has transformed into a somewhat global organization with a presence across 13 European countries. The CTG acquisition extends presence into North America and delivery capabilities in India and Colombia. Belgium represents about half of Cegeka’s business.

Cegeka offer a wide portfolio of services that spans the entire IT scope. They are only one of three companies (the others being Atos and Capgemini) who are represented on all four squares in our study.

Cegeka’s core value has been “in close cooperation” which is reflected in the new tagline “Shaping Digital Together”. They strive to differentiate from competition on proximity & cultural fit. Cegeka is particularly active in the mid-market and lower end of the upper market. Public/Social and Healthcare are their two biggest areas combined with a strong market share at smaller banks and insurance companies.

With NSI, Cegeka have a strong Francophone connection with 200 people across Luxembourg, Wallonia, France and Canada. Cegeka’s strong local capability is supported by nearshore in Romania, Moldova, Greece and a small footprint in India through CTG.

Over the last 30 years, Cegeka has grown both organically and through acquisitions. They are now betting on the trinity of 5G, AI and cloud to drive their growth for the next decade. They are a partner for Digital Flanders for both Digital Workplace and Applications services.

Applications & Digital

Cegeka appears as a Strong Contender with an impressive CSAT of 3.80. They offer a wide range of applications and digital services through their different divisions: Applications which is primarily software development on Java and .Net working in a natively agile way; Business Solutions which offers strong capabilities on Microsoft Dynamics and Power Platform; Data Solutions with 400+ people offering data and AI related capabilities; and, Professional Services which offers enhanced staffing. Through its digital platforms such as nexushealth and Smartschool, Cegeka is deeply embedded into the local society.

Cloud and Datacenter

Cegeka has a very strong hybrid cloud capability with a service offering covering public cloud (Azure), private cloud solutions (they run datacenters in multiple countries) and edge computing. They have over 2000 employees across 10 countries. The Dexmach acquisition in 2022 gave them very strong capabilities on the Azure platform. Hybrid cloud is a key focus area and they have developed strong assets such as the Horizon observability platform and Kubeport, a cloud agnostic managed container. They appear as a Strong Contender with a CSAT of 3.84.

End User Services

Cegeka offer digital workplace, service desk and ITSM services with a primary focus on Microsoft solutions. Cegeka manages more than 50k digital workspaces across 360 clients. While they have strong capabilities, they do not have the global coverage of the rest of their peers.

Cybersecurity

Cegeka has a comprehensive security offering which covers security operations (SOC and NOC), secure networks, I&AM, and advisory. They recently opened their latest SOC in the US. Their security observability dashboard incorporates AI capabilities and automation enabling rapid threat detection and response across the customer’s IT landscape. The acquisition of SecurIT brought strong I&AM capabilities and they are working to expand their security portfolio and coverage from IT towards also OT.

Main Sectors

-

Medium & small enterprises

-

Public-Social, Healthcare

# Contracts

48

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

✓

POSITIVES

-

Strong local presence and cultural fit

-

Strong hybrid-cloud capabilities

-

Proximity to leadership and local focus

NEGATIVES

-

Limited offshore capability

-

Limited presence in Applications Support

-

Gaps in capability in certain domains e.g. SAP, Salesforce

CGI is a Montreal headquartered global IT and business consulting firm with 94,000 people working on 400 locations around the world. This year marks the 50th anniversary of this global company that started as a two-person operation in Quebec City. Its revenue for FY 2025 was €9.85 bn (growth of 4.6% over the last year) and a healthy book to bill of 1.1. CGI offers end-to-end services from business and IT consulting, systems integration, managed services (both IT & BPO) and IP based services (platform-based services). A key differentiator for CGI is its broad industry clientele. It services customers across financial services, government, manufacturing, retail, communication, utilities and health sectors.

CGI’s business is almost equally split into operations, 55% (both IT and business process) and business consulting and systems integration, 45%. They offer advanced analytics, cloud and IT modernisation, cybersecurity and digital transformation services. CGI works with customers through a local relationship model that is complemented by the global delivery network. They operate a higher onsite mix relative to other IT service providers, 60% of customers are in client proximity while 40% are in global delivery centers.

CGI has long-standing and focused practices across all industries sectors. Their industry experts offer a combination of business knowledge and technology expertise that helps them solve client challenges. CGI has also been experimenting with communities of practices (CoP). The aim of CoP is to bring together practitioners from emerging practices and build internal expertise that can support delivery in these emerging areas. One such initiative is the AI CoP, with the intent to enhance employee knowledge and capabilities on AI.

CGI has a large footprint in Europe with more than 40% of revenues generated here. Belgium is part of the Western and Southern Europe region which contributes to almost 16% of overall revenues. In Belgium majority of the work delivered by CGI is systems integration and implementation projects. However, CGI wants to increase its share of managed services work through account expansion initiatives. Utilities (22%), Retail (18%), Financial Services (14%) represent the industry mix of its customers in Belgium.

Applications & Digital

Though CGI has a global scale and presence, in there Belux market they come across as very niche and local. Their client proximity approach suits customers operating in niche areas. Some of the delivery is augmented by nearshore centre in Portugal. Some of the surveyed customers appreciated the delivery capabilities of this nearshore centre. Clients have praised CGI personnel for their deep technical competence and domain knowledge. CGI score consistently high on CSAT in our survey and this year came out a 3.93 (down from 4.0 last year). They sit within the Challengers section.

Main Sectors

-

EU, Manufacturing,

Telecom, Utilities

# Contracts

6

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

End User

Services

Cybersecurity

POSITIVES

-

Strong business understanding & consulting capabilities

-

Specialization in agile delivery models

-

Competent local teams working hand in hand with clients

NEGATIVES

-

Limited presence and impact in Belgium

-

Limited large managed IT services contracts in Belgium

Cognizant is a global IT services and digital transformation company with 350,000 employees across 50 countries and annual revenues of $19.7 bn (up 2%). Born as the IT development and maintenance arm of Dun and Bradstreet in 1994, it was spun off as an independent company and since then has grown in size to be many times its original parent. Cognizant is especially strong in Financial Services and Healthcare – they work for all top-30 pharma companies and 9 of the top 10 European banks. Products & Resources follows closely, followed by CMT. With acquisitions of several digital agencies they have strong capabilities on UX, digital experience and platforms.

They have now been growing for 5 consecutive quarters with Q3 FY25 growth of 6.5%. North America still represents a large portion of their revenues at 74% with Europe at 20%. Voluntary attrition which was an issue in post-COVID times is controlled is in the range of 14-15%.

In Belgium, Cognizant has a strong presence in Banking and Healthcare sectors and a growing presence in Industry. They have strong local leadership in Belgium focusing on account management and delivery, with 500 local associates and a strong global delivery network.

Applications & Digital

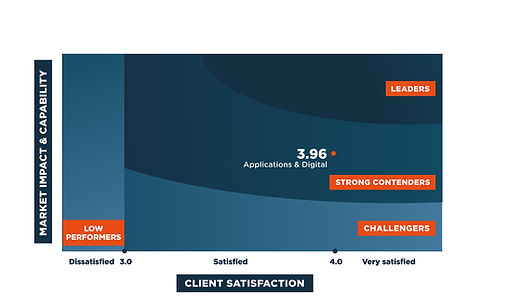

Cognizant offers application modernization and application management services for leading enterprise platforms and technology stacks. This is backed by deep industry expertise particularly in financial services and healthcare verticals where Cognizant works for most leading companies in their domain. In BeLux they are particularly strong in data management and analytics with several happy clients. CSAT for Applications and Digital services has been traditionally strong, but this year they have improved further to 3.96 (up from 3.85 last year) –giving them the highest score of any service provider on this square.

Cloud and Datacenter

While they do not feature on our local square, Cognizant offers cloud and datacenter management capabilities globally. They have 20,000+ cloud practitioners helping clients in across the entire lifecycle. Through their Skygrade platform they offer cloud migration, cloud modernization and multi-cloud management skills. They have strong competencies on both Azure and AWS.

Main Sectors

-

Large & Medium enterprises

-

Financial services, Lifesciences

# Contracts

13

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

End User

Services

Cybersecurity

POSITIVES

-

Strong domain expertise in financial services and healthcare

-

Consistently high CSAT for Applications

NEGATIVES

-

Low local footprint outside of Applications and core domains

Computacenter is a UK headquartered global technology and IT services provider helping customers to source, transform and manage their IT infrastructure. They employ 20,000 people working across 22 countries. In FY’24 Computacenter had revenues of £7bn (up 2.9%) of which technology sourcing was £5.3bn, professional services £778mn and managed services £860mn (down 5.3%). In 2024 they had 192 major customers (defined at gross profit >1mn) with 27% of them being with Computacenter for over 10 years. Average length of service across the group is an enviable 9.4 years.

They have 3700 service desk agents, 5000 engineers and technicians, 2200 project and service delivery managers and 1600 consultants. They are amongst the best technology sourcing companies with particular strength in procurement and logistics, as this is a key focus. They have an ability to provide their value-added reseller services to customers across 70 countries worldwide.

They sell to customers in 8 markets - UK, Belgium, Netherlands, Germany, France, Switzerland, US and Canada and have nearshore / offshore operations in another 8 countries across the world offering 24x7 support, from where they support 5.3mn devices. Their mature global integration centers allow them to deploy technology at scale.

End User services

While they have a broad portfolio of services that include cloud-datacenter, network and security services, it is for enduser services that they really standout. This come out with a very high market impact score and a best-in-class CSAT of 4.08 making them one of the top companies in this space. We rank them amongst the highest on capabilities and they miss out on being a Leader due to lower BeLux revenues compared to their competitors.

Main Sectors

-

Manufacturing, Healthcare, Financial Services

# Contracts

6

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

End User

Services

✓

Cybersecurity

POSITIVES

-

Leader with high CSAT on EUC

-

Best in class capabilities on Procurement and Logistics

NEGATIVES

-

Limited impact beyond EUC

Founded in 1991, the Cronos group has grown to 9500 individuals and €1.3bn in revenues serving 5000+ customers in BeNeLux. The group strategy is to select technologies and actively form independent competence centers. Today they have more than 650 such companies. The group is also an early stage investor and incubator. While the group keeps a low profile some of the brands like Flexso and Cloudar are better known. The combined entity is the largest IT services company in Belgium, a phenomenal achievement.

Cronos is typically active in the small and medium enterprises. Clients work with Cronos for projects and individual excellence of their “knowledgeable and likeable” employees. Cronos is the go-to partner for many clients who need point expertise in niche areas.

The strength of the independent competence center model also comes with some weaknesses: lack of integrated value propositions across Cronos entities and competing agendas at the same client. Also, they struggle to deliver larger managed services at scale. But hey, they have chosen a niche, and they are very good at that. No wonder then that we increasingly see many organizations choosing to add Cronos in their strategic service provider mix.

Applications and Digital

Cronos offers varied application development and digital transformation capabilities across several application domains - ERP, CRM, front-end development, cloud native development, data and analytics, etc. In addition, they offer digital marketing, eCommerce, ITSM and enterprise architecture capabilities. Customer feedback has dropped compared to recent years at 3.50 (down from 3.81 last year). They sit within the Strong Contender’s category.

Cloud and Datacenter

This year we did not have the minimum number of 5 datapoints to place them on our square.

Cybersecurity

This year we did not have the minimum number of 5 datapoints to place them on our square.

Main Sectors

-

Small and Mid-tier companies

-

Public Sector

# Contracts

24

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

End User

Services

Cybersecurity

POSITIVES

-

Good cultural fit: local, easy to work with, deep skills

-

Strong technical competencies and project execution

-

Access to skills in niche and emerging technologies

NEGATIVES

-

Inability to drive an integrated value proposition

-

Weakness in global delivery and managed services

-

Competing agenda of various competence centers

Delaware is a Belgium based international technology services company that is focused on the mid-market segment. They have revenues of $500mn+ globally with exceptional growth in the last few years. They have a presence in 19 countries across Europe, US and Asia. Belgium represents about half of their global business. 2025 saw a new office in Switzerland.

Delaware has an employee strength of 5000+ people globally. They have both offshore (China, Malaysia, Philippines, Brazil, India) and nearshore (Brazil, Hungary, Morocco) capabilities. They are very present in the small to mid-tier segment in Belgium with strong representation within manufacturing and utilities. They are appreciated for their agility, cultural fit, and technical expertise. They have also started to build a management consulting practice with competences in Finance, Supply Chain, HR and Digital solutions.

Applications and Digital

Delaware offers broad based IT services around applications - primarily applications development and modernization, cloud transformation, and communication & collaboration. They have chosen to focus on a few selected platforms where they have built deep expertise. These are Microsoft (Dynamics, M365), SAP, Salesforce and OpenText. They have good capabilities on Mendix. Their applications business is primarily project based today, but they start to expand on managed services. In December 2025, Delaware joined the SAP PartnerEdge program for MSPs with a focus on discrete manufacturing and healthcare. They sit within the Strong Contenders category with an average CSAT of 3.68 (similar to 3.72 last year).

Cloud and Datacenter

Delaware offers both on-prem and cloud based services covering advisory, cloud migration and infrastructure operations. They have strong capabilities for both Azure and AWS. While most of their business is project based, they do offer managed services for the small and medium clients in a flexible way. They sit in the Challengers category with a CSAT of 3.6 (down from 3.8 last year).

End User Services

Delaware does not offer a full DWP solution but rather focusses on providing communication and collaboration services based on the Microsoft 365 suite. They have a strong local team and competencies with outstanding client feedback. They provide both implementation services and managed services and clients praise their future vision for the digital workplace. They had a high CSAT score of 3.80 (down from of 4.13) and sit within the Challengers category.

Main Sectors

-

Small and Medium enterprises

-

Manufacturing, Utilities

# Contracts

23

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

POSITIVES

-

Strong on SAP and Microsoft with deep technical skills

-

Good local presence driving strong relationship at customers

-

Partial FTE model works well for the small to medium sized customers

NEGATIVES

-

Scale and global reach is limited

-

Managed services not at par with competition

Deloitte is a global Tax, Audit, Business Consulting and IT services organization with revenues of $70.5 bn in FY2025 (up 4.8%), with EMEA representing 31% and Technology & Transformation representing $33.4bn. They have 473,000 people worldwide and work with 90% of the Fortune Global 500 companies. Brand Finance has consistently recognized Deloitte as the strongest and most valuable commercial services brand in the world. Deloitte’s history spans 180 years and they are present in 150 countries around the world.

Deloitte is one of the largest professional services firm in Belgium. They closed FY’25 at €822mn (up by 0.3%) and employ 5400 people. Technology and transformation represented €302.5mn. In addition, they have strong teams in finance and supply chain / network operations.

Deloitte is praised for its business acumen, consulting and transformation mindset, ability to take the customer together on the journey and very positive relations with the business. They are seen as thought leaders and strategic partners who can combine both the business and technology aspects.

Deloitte is not a company but a global network of independent firms. This has impacted their ability to coordinate across countries in the past. However, they have now announced an international integration of some of their offerings which include SAP services and Technology & Performance. The results or impact of this are yet to be seen.

Deloitte is betting big on AI with 3bn of announced investments and development of an agentic AI product suite (Zora AI based on NVIDIA AI Enterprise) with integration with leading enterprise platforms.

Applications and Digital

Deloitte has strong capabilities in SAP, Salesforce and digital transformation. They are generally quite strong in terms of technology transformation and can blend in their deep business knowledge to drive customer outcomes. This year Deloitte had a markedly improved CSAT score of 3.76 (up from 3.26) for Applications and Digital services, across 8 evaluated clients.

Cybersecurity

Deloitte does not feature on our Cybersecurity square as they did not meet the minimum threshold of 5 datapoints in our survey. But they do have one of the strongest security advisory practices globally. They also offer a decent MDR solution from nearshore. A few customers who gave feedback, talked about a strong advisory and GRC practice locally with strong assets and an ability to balance risk with pragmatism.

Main Sectors

-

Large & Medium enterprises

-

All sectors

# Contracts

12

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

End User

Services

Cybersecurity

POSITIVES

-

Strong consulting mindset and business understanding

-

Their business model still affords the right attention to Belgium

-

Ability to engage and drive both business and IT stakeholders

NEGATIVES

-

Weaker global delivery model and ability to act as one global company

-

Limited portfolio of IT services

DXC is a global applications, digital transformation and infrastructure/cloud services company with $12.9 bn in revenues (decline of 4.6%) and 120,000 employees across 60 countries. Under Raul Fernandez as president and CEO, they improved their EBIT, achieved book to bill ratio above 1, maintained a good cash flow and reduced overall debt. Given that this has been achieved in a very difficult market environment, these are clear signals that DXC is finally turning the corner. A return to profitable revenue growth will be a fantastic crowning achievement, although its likely to be elusive in the next couple of years.

Last year DXC re-organized into service lines. Global Business Services (GBS) was split into Consulting & Engineering Services (CES) which comprises its applications business, and into Insurance where DXC is a leader in providing specialist software and services serving 21 of the top 25 insurance companies worldwide. The third service line Global Infrastructure Services (GIS) comprises of hybrid cloud, digital workplace and security services.

DXC have close to 1000 people in Belgium and are a key player particularly within the government sector. In BeLux GBS represents 75% of the business.

Applications and Digital

DXC wants to focus on building modern applications on a secure cloud platform. They are proving that in BeLux with innovative solutions for their customers leveraging the newest technologies. They are a key player within the government sector where they have strong credentials on digital transformation for the citizen. They support their many clients in all areas: front-end, back-end and organizational change management. This year they had a CSAT score of 3.51 (consistent with last year) across 12 clients. They sit within the Strong Contenders category.

Cloud and Datacenter

DXC provides cloud advisory and migration and on-premise and public cloud services with half a million virtual servers under management. They have 38,000+ certified cloud professionals on the leading public cloud platforms. This year they had a CSAT score of 3.27 across 8 clients (consistent with last year), which pushes them into the Strong Contenders category.

Main Sectors

-

Large & Medium enterprises

-

Government

# Contracts

20

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

Cybersecurity

POSITIVES

-

Strong digital transformation skills

-

Strong in custom applications development and digital transformation

-

Very strong in the government sector

NEGATIVES

-

Limited presence outside of the public sector

-

Global revenues still shrinking

This is the second year of having Econocom on our End User services square, for which they have one of the biggest revenues on the local market. Econocom is a French headquartered European IT services company with €2.7bn in FY’24 revenues (growth of 3.6%), 8450 people and a presence across 16 countries. In the end user services space, Econocom is one of the few companies who is able to combine deployment and ongoing management of equipment with a comprehensive set of purchasing, reselling and leasing services.

After a strong period of growth until 2017, Econocom plateaued in revenue. This year they have grown 5% at the end of the first three quarters. As part of their strategic 2028 plan, their ambition is to grow to €4bn with growth in each of the regions and a strong growth in Germany. Though it is difficult to see how that can be achieved by organic means only.

Econocom’s main service offerings globally comprise of Equipment (products & solutions) comprising (45%), financing (37%) and services (18%). This year they carved out a 4th dedicated service line AudioVisual where they aim to be a European leader for meeting rooms and unified communications.

They have built a strong portfolio of services around workplace services (65%), the other being infrastructure and network (15%) and audiovisual and digital signage (7%). Locally in BeLux they have a more balanced portfolio with an equal split across resell, financing and services.

Econocom delivers services for clients in France, Spain, Belgium and Netherlands and offer distribution & financing services in 16 countries. They have strong nearshore delivery capabilities in Morocco from where they deliver workplace services, though quite some of the clients participating in our survey had mostly local teams.

End User Services

Most of Econocom BeLux’s service portfolio comprises end user services where they deliver service desk, workplace and field services backed up by their strong financing and distribution business. They have a strong footprint in the public sector. They are a good choice for companies looking to source a European footprint, but they lack the global presence of their competition. They had a good client satisfaction score of 3.65 (slightly lower than last year’s score of 3.70). They appear as a Strong Contender on the square.

Main Sectors

-

Public institutions

-

# Contracts

5

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

End User

Services

✓

Cybersecurity

POSITIVES

-

Full spectrum offering across resell, finance and services

-

Strength and focus on workplace services

NEGATIVES

-

Lack of a global footprint

-

Need to strengthen managed service offering

Fujitsu is a global technology services company with 113,000 employees and IT services revenues of $14.5bn. 71% of their revenues come from Japan, while Europe represents 18%. They are truly global with a presence in over 180 countries. Sustainability is high on their agenda with their global mission statement being - to make the world more sustainable by building trust in society through innovation.

Fujitsu provides hybrid IT and cloud services, digital workplace and service desk, network management and security, and a niche set of application services. With Fujitsu uvance, they want to offer eco-system solutions to meet global sustainability objectives. In industries such as retail and healthcare, Fujitsu offers end to end solutions spanning applications, hardware and devices.

In April 2025 Fujitsu reorganized its business from global business groups and region Japan to two industry focussed organizations: Enterprise Business (Manufacturing, Distribution & Service) and Public Business (Finance, Public and Social Infrastructure). We believe this reorganization breaks through geographic barriers (Japan vs RoW), is aligned with the uvance mindset of global industry solutions, and allows healthy competition within the group to develop and grow a business line (not always Japan).

Fujitsu has 650 people in Belgium and another 700 working from global delivery centres for Belgian clients. Almost half of Fujitsu’s business comes from the European institutions and government sector. They are a strong fit for mid-market clients who appreciate their flexibility and culture alignment. Within the industry, while we see them often in the European arm of large Japanese conglomerates.

Applications and Digital

Fujitsu’s application expertise in Belgium is centered around two key capabilities – Blockchain and ServiceNow. They have a global Blockchain CoE in Belgium with several projects for European and global clients. They also have a strong ServiceNow practice with 60 consultants locally. This year they did not have sufficient datapoints to be on the square.

Cloud and Datacenter

Fujitsu provides both on-premise and cloud infrastructure management services by leveraging their local and nearshore / offshore delivery capabilities under their hybrid IT service portfolio. While they have strong capabilities for Datacenter, at par with the top players, the scale is not the same as the peers putting them into the Challengers category. Also while they have the global capability for cloud services, we do not see sufficient datapoints locally yet.

End User Services

Under their Work Life Shift portfolio, Fujitsu provides AI driven digital workplace and service desk activities. Their 16,000 people support 3 million+ end users and 14mn devices through 8 delivery centers across the world. This year they had an average CSAT of 3.43 and sit high within the Strong Contenders category.

Main Sectors

-

Medium & Small enterprises

-

EU, Government, Industry

# Contracts

11

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

POSITIVES

-

Flexible, client centric approach

-

Strong fit for mid-market clients

-

Ability to offer end to end digital solutions

NEGATIVES

-

Weaker presence outside of European institutions and Japanese companies

-

Low cloud footprint in BeLux

Hexaware is an IT consulting and services firm with $1.43bn in revenues (up 13.7%, Europe growing by 3%). They have 32,000 employees with offices in 19 countries who serve 370+ customers. Europe represents about 20% of their revenues. 2025 saw the successful IPO of the company, the biggest IT services IPO in India in the last decade.

They have expanded their previous 4 service lines into: Digital & Software, Data & Analytics, IT operations, Cloud, Enterprise platforms, BPS, AI and even a separate service line for setting up GCCs.

While they offer services for all major industry sectors – their two most important verticals are Banking & Financial services and Healthcare & Insurance which together form 50% of their revenues. In Belgium, Hexaware is particularly active in the Insurance sector where they work for all the major insurance companies. This year also saw the acquisition of Cybersolve bringing a strong capability and solutions within I&AM.

While Hexaware offers a full-service portfolio across applications services, cloud and infrastructure and BPO we find them particularly strong in RPA / automation and testing services. They have developed specific solutions such as PaymatiX – a banking specific DWH offering and Amaze which is their platform for cloud migration and transformation.

While they have consistently set a high satisfaction score at their long-term clients, they seem to be unable to move up the value chain to grab more market share at those clients and become strategic or primary partners.

Applications and Digital

Hexaware offers digital transformation, applications management and development capabilities on different technologies and application platforms. Their enterprise platforms cover SAP, Salesforce, Adobe, ServiceNow amongst others. They have consistently had a high CSAT score in our survey and came in at 3.83 (same as last year).

Main Sectors

-

Insurance

# Contracts

5

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

End User

Services

Cybersecurity

POSITIVES

-

Consistently high client satisfaction

-

Very strong presence in the Insurance sector

-

Good feedback on RPA and Testing

NEGATIVES

-

Unable to scale up at long term clients

-

Need to grow the business outside of Insurance

HCLTech is a global IT services company with annual revenues of $14.2 bn (up 4.6% in the last quarter) and 227,000 employees across 60 countries. Over the last 4 years, HCLTech has been the fastest growing Indian IT services firm in their league. They are organized into the following business segments: IT & Business services (74%), Engineering & R&D services (16%), and Products & Platforms (10%). Europe represents 27% of their global business.

On the 25th anniversary of the HCLTech IPO in 2000, they have revealed some truly remarkable figures highlighting the success of the company. Every Euro invested in the year 2000 would have been multiplied by x62 over the last 25 years (based on share price of 10 Jan 2025 and considering dividend payouts).

HCLTech has a wide portfolio of services across applications, cloud/infrastructure, digital workplace and BPO with sizeable business in each of these areas. They are amongst the leaders for provision of engineering services. Platform solutions such as HCL Notes, Domino and Unica provide certain stickiness with their customers. Clients appreciate HCLTech for their knowledge, service delivery, flexibility and willingness to work together with a positive mindset.

Application and Digital

This year marks the debut of HCLTech on our Applications square. While they have limited clients in Belgium & Luxembourg, they have market leading competencies across applications management, development, modernization and testing. Applications business constitutes close to half of their global business. They use their AI Force platform to enhance the software development lifecycle and drive efficiencies and outcomes for their customers. They had an excellent CSAT of 3.81 on their debut.

Cloud and Datacenter

HCLTech offers comprehensive cloud migration, cloud operations and cloud native development capabilities. While they don’t have the market share of the leaders in BeLux, they have a small number of clients who are top names within their industry. They have a public cloud first mindset. They have an agreement with Proximus’ Enterprise Business Unit to focus on the small and mid-tier market for the provision of hybrid cloud services. This year they had a client satisfaction score of 3.83 (up from 3.43 last year) and sit within the Strong Contenders category.

End User Services

While HCLTech does not make it to our end user services square locally, we believe they are one of the global leaders for end user services with some of the strongest capability in this domain. They have 30,000+ people working for 400+ clients, managing more than 15mn devices. HCLTech offers service desk, digital workplace, mobility, collaboration and field support. They are recognized by Gartner as a Leader in this category. They have partnerships with leading software companies and hardware vendors.

Main Sectors

-

Large & Medium enterprises

-

All sectors except Public

# Contracts

13

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

Cybersecurity

POSITIVES

-

Strong cloud transformation capabilities with cloud first mindset

-

Ability to offer all services for a CIO

NEGATIVES

-

Limited local client footprint compared to competition

-

Lack of local workforce and presence on the ground

Inetum is European IT services, software solutions and value-added reseller with annual revenues of €2.4bn in 2024. While they are present in 19 countries and have global service centers across Europe, Africa, South America and Asia, majority business is in the four countries of France, Spain, Portugal and Belgium. Inetum is owned by the Bain Capital PE group. They have 27,000 people globally of which about 4000 people at offshore-nearshore locations.

Inetum have a long history in Belgium via their acquisition Real Dolmen which they acquired in 2018. They employ about 1200 people in Belgium. Inetum is in midst of a transformation from being a local service provider with strong cultural fit and localized services, towards delivering managed services from local and nearshore locations. While there are benefits in terms of costs, skills, industrialization and scalability, the model goes against the very local essence of Real-Dolmen, which was why many clients chose to work with them in the first place, creating some challenges.

The clients of Inetum are often found in the public sector or the SME segment. This year they appear on 3 out of the 4 squares, barely missing out on Cybersecurity. Inetum is a strong value-added reseller – amongst the top locally.

Applications & Digital

Inetum performs application development, application modernization and also operations. Inetum’s capabilities span Java and .Net, full stack development and data services on the Microsoft stack, and platform solutions such as SAP, Microsoft, Salesforce, ServiceNow. Inetum is appreciated for the people skills, cultural fit of the consultants and project execution. At the same time there is feedback of a capacity sourcing mindset (as opposed to managed services).

Cloud and Datacenter

Infrastructure services has traditionally been the backbone of their business in Belgium. Inetum can expertly manage your IT infrastructure or datacenter, provide a private cloud solution from their own datacenter, or provide public cloud services on the Microsoft Azure platform. These services can be delivered both locally and increasingly from nearshore.

EUC

They deliver both workplace and service desk services including the resell for laptops and other equipment. They have been working at the Flemish government and bpost for several years. They offer a multi-lingual service desk capability from Casablanca.

Cybersecurity

Inetum has a wide security portfolio covering prevention, detection and response services around application, infrastructure and network components. The primary service is a 24x7 Inetum SOC in Spain. Inetum also provides advisory services around security compliance on NIS2 or DORA.

Main Sectors

-

Small & mid-tier

-

Public sector, Utilities

# Contracts

35

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

POSITIVES

-

Strong local partner for mid-market and public sector

-

Broad capabilities in all areas

NEGATIVES

-

Operating model transformation presents challenges

-

Need to mature managed service offering for applications

Infosys is a global technology services and digital transformation company with $19.7 bn revenues (FY25) and revenue growth in Q1 and Q2 FY26 being 3.8% and 2.9% respectively. The company operates at a healthy operating margin of 21%. It is the 2nd largest IT company in India by market cap and employs 330,000 IT professionals. The top 25 clients at Infosys contribute to over 35% of revenue, underlining their focus on managing and growing top customers.

Infosys has set its focus on two strategic areas – AI led transformation and cloud transformation. Topaz is a set of AI-first services, solutions and platform that uses Gen-AI technologies to drive business value. With 250k AI aware employees and an assistive AI platform, Infosys is well positioned to support customers in their ongoing AI initiatives.

Revenues from Europe represent 30% of global revenues. In Belgium they have some long-term key customers like Proximus, Toyota and Telenet and are well diversified being in all sectors except public/EU.

Applications & Digital

Infosys continues to be a strong player in AM/AD and systems integration. We consider them to be the strongest Indian company for large systems integration programs. Their strength emerges from strong proficiency in agile development, process efficiency and integration of GenAI capabilities into application lifecycle. Customers appreciate Infosys for quality of delivery, account management and client centricity. Infosys had a client satisfaction score of 3.64 (down from 3.85 last year).

Cloud & Datacenter

This year marks the debut of Infosys on the Cloud and Datacenter square. Unfortunately, they sit in the Low Performers category due to challenges at a couple of clients. Infosys have a strong capability around cloud and datacenter with several large European clients. This is powered by the Infosys Polycloud platform, a hybrid cloud management platform that enables delivery of cloud services across multiple cloud platforms. This year they had a CSAT of 2.94 across 5 clients.

Main Sectors

-

Large enterprises

-

Teleco, Manufacturing

# Contracts

23

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

POSITIVES

-

Long established client relationships in Belgium

-

Deep industry knowledge and capability

-

Strong account and relationship management teams

NEGATIVES

-

Vertical Europe wide P&L structure leads to lack of a country focus

Kyndryl is the world’s largest provider of infrastructure services. With 4400+ customers including 75% of the Fortune 100, Kyndryl continues to be the preferred partner for mission-critical managed infrastructure and transformation projects. Kyndryl manages approximately 6.2 million MIPS (Million Instructions Per Second), representing over 50% of the managed mainframe market. They have 73,000 employees with key hubs in India, Poland, Brazil, Japan, Czechia and Hungary.

Kyndryl ended 2025 with revenues of $15.1bn (down from $16bn in 2024). Revenue has continued to decline since several years. However, EBIT has continued to improve and FY’25 saw a sharp upturn in net profit, landing in positive territory for the first time. FY’26 revenue guidance is a 1% growth, which would be a remarkable turnaround for this remarkable company. Kyndryl’s has followed its 3A growth strategy – Alliances (with hyperscaler to drive cloud revenues), Advanced Delivery (strengthened automation via Kyndryl Bridge) and Accounts (focus on key accounts and improving profitability).

Kyndryl’s core offerings are cloud (34% of revenue) and core enterprise and z-cloud (30%). Other services include Security & Resiliency (14%), Application, Data & AI (7%), Network & Edge (8%) and Digital Workplace (7%).

In Belgium they are one of the largest IT services companies.

Cloud & Datacenter

Kyndryl builds and provides managed services for customers’ multi-cloud environments. Kyndryl has 41,000 certified cloud consultants to deliver critical managed service operations and transformation projects onto cloud. They have a best-in-class service delivery and governance framework underpinned by Kyndryl Bridge’s AIOps that is built on open architecture and seamlessly integrate all hyperscalers. They have long-standing customer relationships and are one of the most mature in Cloud operations. They have consistently had a high CSAT and this year have broken the 4 threshold to end up at a CSAT of 4.03, the highest for this square. They are once again the only Leader for this square.

Cybersecurity

While they do not feature on our Cybersecurity square due to lack of sufficient datapoints, they have a very mature global capability. They have 7500 security consultants globally and a comprehensive security portfolio across Assurance (advisory, GRC, threat hunting), MDR, MFA and network security and incident recovery services.

Main Sectors

-

Financial Services including banks and insurance companies

-

Manufacturing, Retail, Government / EU

# Contracts

16

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

✓

End User

Services

Cybersecurity

POSITIVES

-

Leader in complex infrastructure / mainframe services

-

Strong hybrid cloud capability with own datacenters with shared solutions

-

Long standing customer relationships across industry segments

NEGATIVES

-

Several scope dependencies on IBM in certain areas (particularly linked to consulting and applications)

NRB is a Belgium based IT services company with revenues of €638mn in 2024 and having over 3670 employees making them one of the largest local players. NRB offers full range of IT services right from application development and management, infrastructure and cloud services and security. NRB offers development services across both custom software and ERPs such as SAP. They have a nearshore center Athens, specializing in mobile and web development. Part of the larger NRB group (which is owned by Ethias) their sister company Prodata is a specialist in providing security solutions.

NRB primarily services the Belgian market, with strong focus on Walloon public sector and European institutions. Their strength in delivering proximity and regulatory compliant services make them a good partner for public sector institutions. International customers are serviced through its subsidiary Trasys International. Going forward NRB wants to not only strengthen its presence in Belgium, but extend its market presence internationally.

NRB is one of five companies to be an all four squares. NRB clients appreciate the local approach and character of NRB.

Applications & Digital

NRB offers end-to-end applications services from development to maintenance. They have strong capabilities in cloud native development (Java, .net, Python), data, mainframe modernization, SAP and Salesforce. NRB achieved a customer satisfaction score of 3.72. This is the largest of their different capabilities. They are a leading partner for the SPW serving the Walloon public institutions.

Cloud and Datacenter

NRB has strong hybrid cloud capability integrating both private and public cloud solutions. They have a best-in-class mainframe and AS/400 capability and are one of the few companies still investing into developing these capabilities. NRB operates three Tier III+ high availability datacenters in Belgium (a new one added in Muizen) and are a suitable partner for the large banks, payroll organizations or any other organization requiring huge computing power situated locally. NRB had an excellent CSAT of 4.0.

End User Services

NRB offers both digital workplace and service desk capabilities to local clients. They offer 24x7 support in English, French and Dutch out of two locations in Belgium. The services are integrated within their security framework built on IBM QRadar, Splunk and the Microsoft Defender suite. While this is a suitable offering for locally situated customers, they are limited in their ability to provide global coverage.

Cybersecurity

NRB is able to offer customers security advisory and implementation, GRC, offensive security, network security, SASE, identity protection and managed security. They have a local SOC offering 24x7 monitoring and a SIEM solution based on Splunk.

Main Sectors

-

French speaking sector

-

Public-Social, Healthcare

# Contracts

20

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

✓

End User

Services

✓

Cybersecurity

✓

POSITIVES

-

Exceptional mainframe capabilities

-

Strong local presence and proximity services

-

Ability to deliver to stringent regulatory and cybersecurity standards

-

Offers end-to-end services from cloud, applications and security

NEGATIVES

-

International footprint remains limited

-

No offshore capability

-

Limited presence outside of the french speaking sector

NTT Data is a Japan-based global IT service provider with revenues of $30bn. For the last 3 years the company has grown at a CAGR of 20% maintaining a health operating margin of 10%. The integration of NTT Ltd with NTT Data makes them a full stack IT provider serving clients across system integration, managed services, and AI. The company has 200,000 employees across 70 countries.

NTT Data works with 75% of the Fortune 500 companies with manufacturing and financial services being the two largest verticals. They are one of the largest service companies in Belgium by revenue with a very impressive client portfolio across manufacturing, financial services, utilities, telecom and the European institutions. They are market leaders in some niche areas such as Network and Telephony.

Cloud & Infrastructure

NTT is the 3rd largest data center provider in the word and operates 80 data centers globally. With the increased proliferation of AI, and demand for sovereign clouds NTT anticipates higher demand for data center operations. NTT is investing over $10 billion in new energy efficient datacenters. The asset-heavy strategy of NTT is contrary to the asset-light strategy adapted by most IT service providers. NTT also has partnerships with leading hyper-scalers and offers clients AI-powered cloud services including multi-cloud management, industry cloud solutions and cloud transformation services. In Belgium, NTT works with several companies architecting, transforming and managing their cloud platforms. This year they had a remarkable improved CSAT of 3.68 (up from 3.04 last year), which brings them into the Strong Contenders category.

Cybersecurity

NTT Data has a mature cybersecurity offering with 49 SOCs and 7500 professionals. In Belux NTT Data has over 160+ security professionals supporting local customers. They offer a full range of security services including managed security services (SOC) and Managed Detection and Response (MDR). They also have partnerships with major security software providers such as Zscaler, Microsoft, SecurityBridge and Qualys.

End User Services

While NTT Data did not feature on our square due to lack of local datapoints, they do have a strong global practice that offers comprehensive end to end services with more than 7000 employees. Romania is the main hub in Europe for multi-lingual service desk and workplace services and is supported by people in India, Mexico, Malaysia, Dalian and Philippines for round the world coverage. They manage 7mn+ users and 11mn+ devices. One of their major customers is BMW for whom they provide multi-lingual service desk for 150,000+ users globally.

Main Sectors

-

Manufacturing, EU, Government

# Contracts

11

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

✓

End User

Services

Cybersecurity

✓

POSITIVES

-

Outstanding capability on Network and Telephony

-

Broad portfolio across DC, cloud, EUC and security

-

Strong relationships with leading hardware and software providers

NEGATIVES

-

Lower market visibility and perception (compared to capabilities)

-

Inconsistent feedback on managed services offering

nviso is a pure play cyber security company based in Belgium. Starting in 2013 with 5 people, it has grown to over 300 cyber security experts. The company has experienced double-digit growth over the last few years. They have now expanded beyond Belgium to Germany and Austria. In 2022 a delivery center was setup in Greece from where 24/7 security operations are delivered. nviso features on our security square as a Strong Contender.

nviso offers full range of security services including Managed Detection and Response (MDR), offensive security, advisory and GRC, cloud & application security. They also offer digital forensics and incident response. They have partnerships with all leading security software providers such as Microsoft and Palo Alto. It is a top-tier partner for Microsoft security solutions. Across Europe they have over 70+ customers which include most of the large financial services customers in Belgium.

nviso continues to invest and strengthen its security offerings. Nitro their security automation platform is deployed at many customer sites. The platform offers 200 automation and playbooks, it integrates seamlessly to various security stacks including Microsoft Sentinel. It enables 24/7 MDR services and real-time threat detection and response.

nviso customers are happy with their service and they get an excellent CSAT of 4.08 (down from 4.18). Customers called out penetration testing as a key area of strength. They like the fact that nviso is transparent on outcomes that can be achieved and generally deliver to their commitments. The advisory and GRC is another area of strength. Clients praise the focus on security and the high skill of their employees. Managed security operations however seems an area where they lag behind some of their larger competition.

Main Sectors

-

Financial Services

# Contracts

5

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

End User

Services

Cybersecurity

✓

POSITIVES

-

High client satisfaction

-

Very good on projects and point security services

-

Focus on security and specialization

NEGATIVES

-

Scalability can be a challenge as more customers are onboarded

-

MDR services not at par with leading competition

Orange Cyberdefense is the cybersecurity division of the Orange Group. They have 3500+ skilled professionals who support businesses in identifying, detecting, and responding to cyber threats. Orange Cyberdefense offers proactive threat prevention, vulnerability assessments, and comprehensive solutions for protection of networks, applications and data. They have one of the most comprehensive and mature security offerings anywhere in the world.

Through their 18 SOCs operating from multiple locations, Orange Cyberdefense specializes in MDR, incident response & digital forensics, OT security, threat intelligence, and managed security services. The Cyber Experience Center in Antwerp simulates real world scenarios with visual storytelling to educate CISOs, CIOs and even the C-Suite. They are one of the few providers that run a SOC in Belgium.

Their AI powered core fusion platform serves more than 50,000 customers across the world. Their R&D team of 250+ researchers and analysts uses AI for dark web surveillance and threat intelligence. 12 CERTs running 24x7 provide forensics and recovery. They have 4 scrubbing centers to mitigate DDoS attacks.

Given their strong capabilities and market share, they emerge as a Leader in our Security square with a CSAT of 3.55 (down from 3.63).

Main Sectors

-

Financial Services

-

Healthcare

# Contracts

6

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

End User

Services

Cybersecurity

✓

POSITIVES

-

Very strong capabilities in threat intelligence

-

Offers comprehensive range of security services

NEGATIVES

-

OCD organization units are siloed and difficult to navigate

-

Still perceived as a telecom driven security company

This year marks the debut of Proximus NXT on our survey. In 2024 Proximus consolidated the IT activities for B2B customers under the umbrella of Proximus NXT. This created a BeNeLux IT company with more than 2000 people that included amongst others the erstwhile business of Telindus, Davinsi Labs and Codit.

Proximus NXT has the following main service lines – Data & AI, Digital Workplace, Advanced Networks, Cybersecurity and Cloud. They focus on the public sector and mid-market segment with organizations that have a large local footprint. Immediately in their first year on the survey, they have come out with flying colours – scoring very well on CSAT and local market impact and capability.

In 2024 they signed a strategic partnership agreement with Microsoft and aim to become a top-3 Microsoft partner in all domains.

Cloud & Datacenter

Proximus NXT offers a complete hybrid cloud portfolio across on-prem, private or public cloud and edge computing solutions. They sold their datacenters to Datacenter United in 2025, through whom they offer local hosting (tier IV datacenters). They have growing public cloud practice across all 3 major platforms with particular strength on Azure. Through Clarence, its JV with LuxConnect, Proximus offers the most mature sovereign cloud solution on the market based on the Google Distributed Cloud air-gapped architecture. Proximus NXT had a CSAT of 3.80 and sit within the Strong Contenders category.

End User Services

While they did not make it on our square due to lack of interviewed clients, they offer workplace solutions including a WPaaS offering, ability to provide audiovisual support (meeting rooms), support telephony / communication, and support M365 and Teams. They are a partner of choice for local mid-sized clients needing localized support.

Cybersecurity

Proximus NXT ends up as a Leader on this year’s Cybersecurity square with an excellent CSAT of 3.82. They have a very mature offering with 350 experts providing a comprehensive scope across data, application, network, cloud and endpoint security. They operate their own 24x7 SOC from Belgium. They have deep capabilities on all leading security platforms and a large number of local customers. They have a strong security advisory practice. In 2025 they won the landmark SECaaS2 contract with the federal government, expected to be worth €100mn over 7 years covering 70,000 users.

Main Sectors

-

Mid-Tier

-

Public sector

# Contracts

17

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

✓

End User

Services

Cybersecurity

✓

POSITIVES

-

Strong local player

-

Comprehensive hybrid cloud and sovereign cloud offering

-

Leader in Security

NEGATIVES

-

Lack of structural offshore capability

-

Limited scale compared to global competition

-

Disconnect sometimes between sales and delivery

PwC is one of the world’s leading professional services companies delivering Audit & Assurance, Advisory services, and Tax & Legal services. They service 86% of the Global Fortune 500 companies and had revenues of $56.9bn last year (up by 2.7%). PwC has over 364,000 people across 136 countries (of which 120,000 in advisory).

Advisory services represent about $24.3bn globally. This includes both business advisory (majority) and technology advisory. In terms of Technology capabilities, PwC offers technology strategy, business application services, cloud, data & analytics cybersecurity, and services on new technologies like AI.

PwC Belgium has a large local presence with 2150 employees and 438.7mn of annual revenues of which 147mn of Advisory services. Advisory comprises of business and technology consulting, deals/M&A. They are well integrated into the local community with several pro-bono and social initiatives.

PwC has invested $2bn into expanding and scaling up its AI capabilities. In 2024 they introduced ChatPwC on a global basis offering a secure and private domain access to all their employees.

Applications & Digital

PwC’s strength lies in their ability to combine a deep understanding of business challenges with the latest technical know-how. They are very strong at designing and implementing digital solutions to business problems. They have strong capabilities in Salesforce and Workday. They continue to have high scores in the Applications and Digital square with a CSAT of 3.74 (down from 3.8 last year).

Main Sectors

-

Very well represented

across all sectors -

Government

# Contracts

5

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

End User

Services

Cybersecurity

POSITIVES

-

Combine deep business understanding and technology

-

Strong local presence and integration with society

NEGATIVES

-

Smaller scale compared to the larger competition

-

Lack of operations footprint at BeLux clients

Stefanini is global technology company with roots in Brazil. It has 35,000 people and presence in over 40+ countries worldwide. It’s revenue in 2024 was $1.4bn. They offer service desk, workplace and infrastructure services, application and digital services and cybersecurity services, with particular strength in end user services that represent close to half the business. In 2025 they announced a reorganization into 7 business units with an ambition to grow the applications business and AI led transformation. While 20,000 of their people are in South America, they have 3500+ employees in Europe.

Brussels is the European HQ of Stefanini and they have delivery centers in Romania, Moldova and Poland. Locally they have 150 consultants in Belgium, who together with the nearshore centers support clients in all European languages. Stefanini is growing at a rapid pace in Belgium where they work with large clients with a European or global footprint. They are particularly strong in the Manufacturing sector.

Stefanini has established a Gen AI center of excellence and has been successfully applying AI solutions in its client engagements. By integrating AI across all its operations, it has elevated the value delivered to customers. The Stefanini AI platform - SAI has built-in capabilities in NLP, machine learning and intelligent automation. SAI is deployable across all 7 core areas of Stefanini including applications, cybersecurity, digital workplace and marketing.

End User Services

Stefanini has demonstrated strong capabilities in End User Services. They have 10,000 people across 10 delivery centres delivering end-user services. Innovative tech solutions such as SophieX (Gen AI assistant) and Chameleon (self-adaptive portal) have helped improve productivity. SophieX performs real-time translations in 40 languages and offers human-like interactions. With a customer focused workforce, strong process and intelligent tools, Stefanini is a top pick for end-user services and we consistently include them in all end user RFPs. They have a top CSAT of 3.99. Customers appreciate Stefanini for their customer focus, service delivery, and cultural fit. They sit high in the Strong Contenders section.

Main Sectors

-

Manufacturing

# Contracts

7

APPLICATIONS

MANAGEMENT

DATACENTER /

CLOUD

End User

Services

✓

Cybersecurity

POSITIVES

-

Consistently top-notch client feedback

-

Client focus and flexibility

-

Strong governance and open communication

NEGATIVES

-

Credentials limited to Digital Workplace and Service Desk

-

Brand visibility needs improvement in Europe

-

Pre-sales effort needs improvement

Sopra Steria is a French headquartered European technology services company with the ambition ‘to become a compelling alternative to global providers for major European clients’. They reported revenues of €5.8bn in FY’24 (flat compared to FY’23) and a 3.8% decline in the first half of FY’25, with close to 51,000 people across 30 countries. France (48%) and UK (18%) are the two largest geographies, with rest of Europe being about 32%.

With the sale of Sopra banking software to Axway, the group now focusses predominantly on digital transformation and systems integration services. They have a very complete portfolio across applications, cloud and infrastructure, data & AI and cybersecurity. At a group level, they have a strong focus on the public sector, defence, aeronautics and financial services which together represent 70% of the business.

The acquisitions of Tobania and Ordina gave Sopra Steria has a developed a formidable presence in the BeNeLux with 4000 employees and €700mn in revenues (close to half of it in BeLux). It also gives them a strong footprint within the manufacturing industry locally. Jo Maes, the BeNeLux lead is part of the global Executive Committee.

End of last year Sopra Steria has been in the national news due to the wrong reasons – the termination of the failed i-Police contract that was awarded to a consortium led by Sopra Steria in 2022.

Applications & Digital

Last year marked the debut of Sopra Steria in our Applications and Digital square. This year we interviewed clients mainly within the financial services industry and public sector. The clients are in general satisfied, with a CSAT of 3.48 (down from 3.74). Sopra Steria is praised for the very strong domain skills within financial services, and a strong local presence and connect. Lack of a strong offshore capability and therefore higher cost is also frequently mentioned.

Main Sectors

-

Financial Services

-

Public sector and European Institutions

-

Industry

# Contracts

8

APPLICATIONS

MANAGEMENT

✓

DATACENTER /

CLOUD

End User

Services

Cybersecurity

POSITIVES

-

Strong domain skills in Banking

-

Tier II player to complement global providers

NEGATIVES

-

Price competitiveness of onshore profiles

-

Lack of a strong offshore / global capability

Part of the Tata group, India’s largest multinational business corporation, TCS is also the largest and most impactful of the Indian IT services companies. TCS has over 590,000 consultants across 55 countries. TCS had FY’25 revenues of $30 bn (growth of 4.2% last fiscal and 0.8% in Q3’26) and an industry leading operating margin of 24.3%. They are also the most visible of the Indian IT services companies both globally and locally. Continental Europe represents 14.3% of their revenues. They have expanded their European presence by adding another center in Bucharest.

TCS has a long history in Belgium with a presence dating back to almost 30 years. They have close to 5000 people working for 35+ very satisfied Belgian customers. This year they became one of 5 companies to be present on all 4 squares.

TCS is praised by clients for their very strong delivery capabilities, their reliability and partner mindset that puts the client first. They are well diversified in Belgium with a strong presence across financial services, manufacturing, retail, CPG, transportation and logistics and telecom.

Applications and Digital

TCS continues to remain a Leader within our Applications and Digital square, with a client satisfaction score of 3.85 (up from 3.48) across 17 clients. They have a broad presence on the Belgian market with market leading AMS capabilities, strongly improved systems integration performance and perhaps the broadest technology footprint on the market. The CSAT has bounced back to TCS-usual levels after a few recent years of dip.

Cloud and Datacenter